Industry Outlook: Moldmaking Disruptors or Differentiators

Today’s positive business cycle creates opportunity for mold builders who are aware of new business models and technology trends.

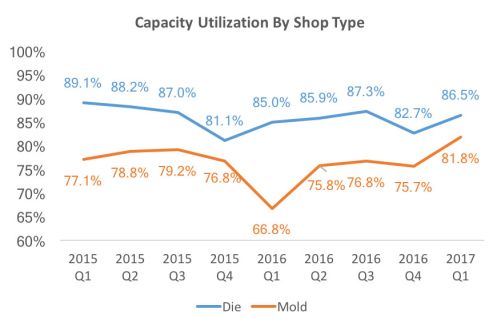

The OESA/Harbour Results Barometer, a quarterly study of the mold and die industry, indicates that for the first quarter of 2017 capacity among mold shops was 83 percent, on average.

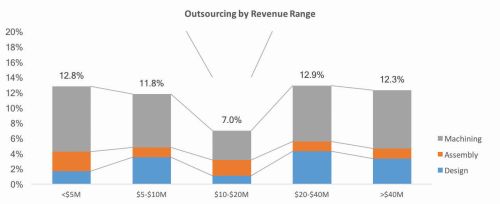

The first-quarter 2017 Barometer survey indicates that mold shops outsource more than 11 percent of new work, of which more than 7 percent is machining. The rest is assembly and design work.

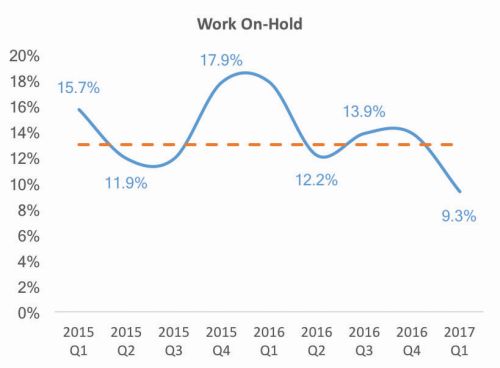

Work-on-hold levels dropped to below 10 percent for the first time since 2015, according to the first-quarter 2017 Barometer.

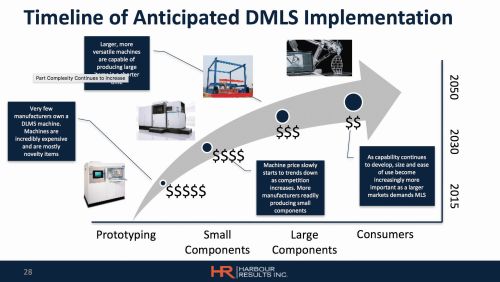

This timeline shows the anticipated implementation of additive manufacturing as it continues to penetrate the moldmaking industry.

Many manufacturers are facing potential challenges as well as opportunities with the new government administration and its interest in renegotiating NAFTA, changing other free-trade agreements, improving corporate tax rates and potentially starting a “trade war” with China. With that being said, 2017 started off with a bang for the mold and die industry. Many shops have since been at or above capacity, which is not too surprising considering the number of economic factors supporting this positive business cycle.

For example, recent market studies conducted by both LMC Automotive and the Manufacturers Alliance for Productivity and Innovation (MAPI) forecast that production in the automotive, appliance, mining and medical industries will be up year-over-year from 2016 to 2017. Additionally, the Purchasing Managers Index shows a significant upswing in manufacturing activity, based on new orders, inventory levels, production, supplier deliveries and the employment environment. These positive economic signals could be attributed to a number of factors depending on the industry, including improved consumer confidence and modest improvements in the oil and gas industry. Overall, it is a positive sign for the mold industry.

On top of those reports, the first quarter 2017 OESA/Harbour Results Inc. (HRI) Barometer, a quarterly study of the mold and die industry, recently assessed 74 tool shops (76 percent of respondents from mold shops and 24 percent from die shops). This study indicated that capacity among mold shops was 83 percent, on average, the highest it has been since the study started in 2015. Additionally, work-on-hold levels dropped to below 10 percent for the first time since 2015.

The same study found that sentiment (a shop’s general business outlook for the proceeding three months) was at 85 percent, which is six percentage points higher than it was at the end of 2016. In this index, 50 is neutral. Increased utilization and lower work-on-hold levels are all building up to a strong 2017. Couple this forecast with the change HRI has seen in the mold business over the years, and you’ll discover a marketplace full of potential growth opportunities, if you are aware and prepared.

For example, HRI has noticed that mold shops have been experiencing a variety of dynamics that are driving the evolution of improved efficiency and cost containment. First, companies are being forced by consumer demand to increase product speed to market. The introduction of new products used to take 18 months, and this is now being accomplished in 10 months, a reduction typical in any market. This reduction in development time is impacting all aspects of the supply chain, including compressed build time for mold shops.

Another factor impacting manufacturing is the drive for companies to grow or maintain market share. This, coupled with the push to reduce manufacturing and development costs, is forcing companies to be more strategic in their business planning, including exploiting specific marketing opportunities to maintain and increase market share, while balancing investment.

All of this creates opportunity for the mold industry through new business models and technology trends. One new business model introduced into the manufacturing space is called the product service system concept, whereby a company leases a product and pays for service and maintenance rather than purchasing the product. It was introduced by Rolls-Royce to service aircraft engines and has been adopted in a number of different industries, including by Xerox for office equipment and Michelin for heavy-duty truck tires.

The three product service system (PSS) models are:

- Product-oriented PSS. Ownership of the product is transferred to the consumer, but additional services are provided.

- Use-oriented PSS. Ownership of the product is retained by the service provider, who then sells the functions of the product.

- Result-oriented PSS. Products are replaced by services. For example, voicemail replacing answering machines.

Many OEMs have adopted these models and are using them to drive revenue. They still own the product, but make money on the lease and service. While we don’t see a huge impact on mold builders at this point, the product service system is a shift in thinking from how OEMs traditionally do business. Fundamentally, any change in how OEMs do business will affect the entire supply chain. It’s too soon to tell exactly how it will impact mold shops, but it’s important to be aware of any changes and adjust business models accordingly. For example, mold shops may want to lease their machines over purchasing them, a decision that could greatly impact overall business planning.

Another new business model mold shops are beginning to adopt is the product-as-a-service provider concept. These types of providers help mold shops meet supply and demand by helping them find jobs to fill their machine tool and/or press downtime or helping them manage overcapacity scenarios. More and more mold shops are looking at outsourcing as a solution to manage overcapacity. In the first-quarter 2017 Barometer survey, mold shops indicated that they outsource more than 11 percent of new work, and just more than 7 percent of that work is machining. The remaining 4 percent is made up of assembly and design work.

An example of a company employing this new business model is MakeTime Inc., which collects profiles of qualified companies and their core capabilities that have available machine time. When MakeTime receives a job request that fits a set of criteria, it sends that job to the matching shop. This ensures the “right job” is going to the “right shop,” delivering profitable business for that machine shop.

This type of service provider concept delivers a number of positive benefits to the industry. First, it allows shops to make the most of its investments by increasing machine uptime. This becomes another way to bring in business beyond traditional relationships and job hunting. Additionally, mold shops will not need to expend additional resources (time and money) to secure more business and generate quotes, and can therefore focus on what they do best: making molds.

Traditionally, mold shops have relied on long-term relationships, working with the same plastics processors over an extended period of time. Today, they can be much more progressive in their processes for landing work. They can look at many different avenues to secure new business, including other mold shops, new industries and even new forums like MakeTime. For example, many shops analyze sales data to identify their best customers and products, and then conduct research to find other, similar companies to target as customers.

The 2017 Barometer study also found that shops with between $5 million and 10 million in revenue handle a bulk of outsourcing from shops with revenues greater than $20 million. A key factor holding many shops back is the ability to keep revenues consistent from month to month. This demonstrates how important it is for mold shops to understand how all revenue streams lead toward better level loading (the process of keeping utilization of the facility relatively even every quarter/month).

Finally, additive manufacturing (AM) is continuing to penetrate the moldmaking industry. Although complex 3D-printing machines are still extremely rare in mold shops, mold builders that invest either directly or indirectly in additive technologies will be better able to differentiate themselves from the competition in the future.

AM provides shops with the ability to prototype parts more rapidly and increase speed to market. It is primarily used by mold shops for prototyping components with unique geometries and very small components. The biggest benefit of AM to mold building is the ability to build cores and cavities using conformal cooling produced with AM technologies, which greatly improve cycle times. For the time being, AM will play a limited role in mold manufacturing, but as the technology evolves and equipment costs decrease, it will likely start to play a larger role.

Mold shops must be cognizant of these new business models and technology trends, as they could be disruptors to the industry or potential differentiators for an individual business. It is important to continue to work on any business, especially when times are good. Mold shops that choose not to invest in new technology, processes and people likely will not be able to survive a dip in the manufacturing industry.

Read Next

Reasons to Use Fiber Lasers for Mold Cleaning

Fiber lasers offer a simplicity, speed, control and portability, minimizing mold cleaning risks.

Read More

How to Use Strategic Planning Tools, Data to Manage the Human Side of Business

Q&A with Marion Wells, MMT EAB member and founder of Human Asset Management.

Read More

Are You a Moldmaker Considering 3D Printing? Consider the 3D Printing Workshop at NPE2024

Presentations will cover 3D printing for mold tooling, material innovation, product development, bridge production and full-scale, high-volume additive manufacturing.

Read More