Computers/Electronics and Medical

Computers/Electronics Industries in Early Recovery and Medical Equipment Output Accelerates

Computers/Electronics Industries in Early Recovery

The Fed compiles and reports data each month that measures the volume of U.S. production of computers and electronics products. This data was recently revised, and the results were, to put it mildly, surprising. As the accompanying chart indicates, total output in this country of computers and peripheral equipment declined sharply in each of the past three years (2009-2011). And the level of total production so far in 2012 is still 25% lower than the output in 2007.

But the good news is that this industry appears poised to start expanding again. In the first quarter of this year, total U.S. production of computers and peripheral equipment is flat compared with the same period of a year ago. The rise will be very gradual at first, but it will start to gather momentum after a few quarters of moderate growth. Our forecast for 2012 calls for an annual increase of 7% in 2012, followed by double-digit gains in 2013 and 2014.

This forecast is based on a continuation of several major trends that affect spending for computer and electronics equipment. First, confidence levels amongst consumers and small business owners are currently rising at a very modest rate, but the trajectory of these data will get steeper later this year and through 2013. Second, access to credit is steadily improving. And third, the production of many of these types of products will be “re-shored” back to America. This re-shoring is due to increases in shipping costs, an appreciation of the Chinese currency, and a desire to shorten supply chains and get production activity closer to the market.

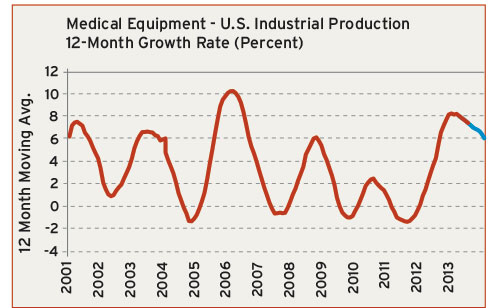

Medical Equipment Output Accelerates

The growth rate in total U.S. output of medical equipment and supplies has accelerated so far in 2012. In the first quarter, production by American manufacturers escalated by nearly 6% when compared with the same period in 2011.The year-over-year growth in 2011 came in at just under 2%, but our forecast calls for an annual gain of at least 4% in 2012. Keep in mind that this is a forecast for the total volume of products manufactured, not the total value of shipments.

This industry has enjoyed stronger-than-average growth when compared with the data from the overall U.S. manufacturing sector, and we expect that this trend will continue for the foreseeable future. This outlook is based on a couple of long-term trends. The most important of these is that many industrialized nations such as the U.S., Japan and most of Europe have aging populations. And technological advances have resulted in an ever-increasing array of medical products for these populations to consume. The other important trend is that access to medical supplies is improving for many of the world’s developing nations. Thus, global demand for medical equipment should continue to rise in the year’s ahead.

The biggest threats to this forecast are: 1) a further deterioration in the economic environment in Europe; and 2) the inability of policymakers in the U.S. to pass legislation that will reform the entitlement programs and reduce the deficit in the federal budget.

Related Content

Editorial Guidelines: Editorial Advisory Board

The Editorial Advisory Board of MoldMaking Technology is made up of authorities with expertise within their respective business, industry, technology and profession. Their role is to advise on timely issues, trends, advances in the field, offer editorial thought and direction, review and comment on specific articles and generally act as a sounding board and a conscience for the publication.

Read More

From Injection Mold Venting to Runnerless Micro Molds: MMT's Top-Viewed June Content

The MoldMaking Technology team has compiled a list of the top-viewed June content based on analytics. This month, we covered an array of topics including injection mold venting, business strategies and runnerless micro molds. Take a look at what you might have missed!

Read More

Steps for Determining Better Mold Prices

Improving your mold pricing requires a deeper understanding of your business.

Read More

MMT Chats: Marketing’s Impact on Mold Manufacturing

Kelly Kasner, Director of Sales and Marketing for Michiana Global Mold (MGM) talks about the benefits her marketing and advertising, MGM’s China partnership and the next-generation skills gap. This episode is brought to you by ISCAR with New Ideas for Machining Intelligently.

Read MoreRead Next

How to Use Strategic Planning Tools, Data to Manage the Human Side of Business

Q&A with Marion Wells, MMT EAB member and founder of Human Asset Management.

Read More

How to Use Continuing Education to Remain Competitive in Moldmaking

Continued training helps moldmakers make tooling decisions and properly use the latest cutting tool to efficiently machine high-quality molds.

Read More

Reasons to Use Fiber Lasers for Mold Cleaning

Fiber lasers offer a simplicity, speed, control and portability, minimizing mold cleaning risks.

Read More