Aerospace & Automotive

Aerospace Outlook: Steady Growth in 2013; Automotive Industry Will Remain a Bright Spot in 2013

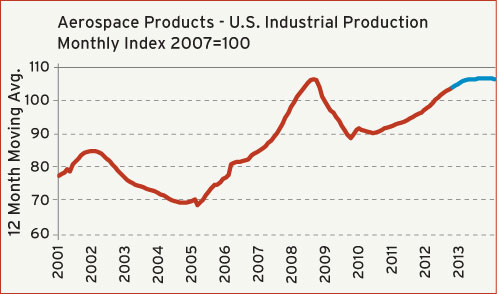

Aerospace Outlook: Steady Growth in 2013

One industry that has not suffered any ill effects from either the uncertainty surrounding the fiscal cliff deliberations or the destruction of Hurricane Sandy is aerospace products. In the third quarter of 2012, total U.S. production of aerospace products and parts expanded by a solid 6% when compared with the previous year. For the year-to-date, output of these goods is up an impressive 8% over 2011. Our latest forecast calls for a rise of 8% for all of 2012 followed by an increase of 5% in 2013.

On the non-defense side, industry consolidation is still a prevalent theme within the industry, and so is energy efficiency. There are still concerns about the long-term profitability for commercial air carriers. Through consolidation, companies are able to eliminate redundancies and re-negotiate unfavorable contracts. This may create some short-term gains, but the best prospects for future profitability rely on improving efficiency. Moving more people at a lower cost is their best hope. This will require investing in newer, lighter aircraft that are manufactured from composite and plastic materials.

For suppliers to the defense industry, the outlook is mixed. It is quite likely that orders for some of the older types of aircraft will be scaled back or even eliminated. But one area that will continue to grow is unmanned aircraft (a.k.a. drones). These aircraft already use a high proportion of plastic and composite parts, and demand for these parts will increase as spending on these types of aircraft ramps up.

Automotive Industry Will Remain a Bright Spot in 2013

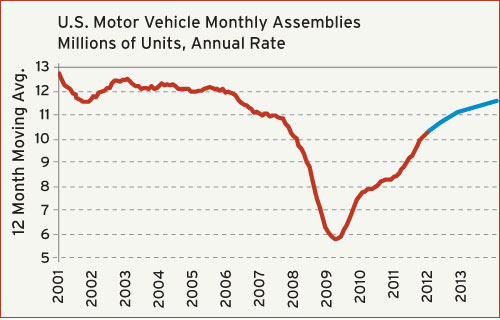

Since hitting bottom in 2009, the automotive industry has been a stellar performer for the U.S. manufacturing sector. In the third quarter of 2012, the total number of motor vehicles assembled in the U.S. jumped by nearly 15% when compared with the third quarter of the previous year. For the year-to-date total car and truck builds are running 22% ahead of the same period in 2011. Our forecast calls for an annual gain of 20% in motor vehicle assemblies in 2012 followed by a 10% rise in 2013.

As the chart shows, the U.S. auto industry has enjoyed several consecutive years of robust growth, but there is still a large amount of pent-up demand in the market. Household income levels have risen very slowly—if at all—during the past four years, and at the same time access to credit has been tight. So the average age of a car in the U.S. is about 10 years. Income levels (along with the employment figures) are slowly rising, and access to credit is gradually getting easier. These improving fundamentals will spur demand for new vehicles for the foreseeable future. The auto industry will also benefit from the long-term trend toward vehicles that are more energy-efficient.

A factor that will amplify the demand for motor vehicles in the short term is the recovery effort in the Northeast that is the result of Hurricane Sandy. A large number of motor vehicles were destroyed during the hurricane, and a large number of additional construction and delivery vehicles will be required in order for these areas to get cleaned up and rebuilt. The effects of Sandy are already showing up as significant increases in the monthly data on vehicle sales.

Related Content

The Trifecta of Competitive Toolmaking

Process, technology and people form the foundations of the business philosophy in place at Eifel Mold & Engineering.

Read More

Leading Mold Manufacturers Share Best Practices for Improving Efficiency

Precise Tooling Solutions, X-Cell Tool and Mold, M&M Tool and Mold, Ameritech Die & Mold, and Cavalier Tool & Manufacturing, sit down for a fast-paced Q&A focused on strategies for improving efficiencies across their operations.

Read More

From Injection Mold Venting to Runnerless Micro Molds: MMT's Top-Viewed June Content

The MoldMaking Technology team has compiled a list of the top-viewed June content based on analytics. This month, we covered an array of topics including injection mold venting, business strategies and runnerless micro molds. Take a look at what you might have missed!

Read More

The Role of Social Media in Manufacturing

Charles Daniels CFO of Wepco Plastics shares insights on the role of social media in manufacturing, how to improve the “business” side of a small mold shop and continually developing culture.

Read MoreRead Next

Aerospace & Packaging

Production of Aerospace Products and Parts is Accelerating; Plastics Packaging Demand Will Exceed Growth in the Overall Economy

Read More

How to Use Strategic Planning Tools, Data to Manage the Human Side of Business

Q&A with Marion Wells, MMT EAB member and founder of Human Asset Management.

Read More

How to Use Continuing Education to Remain Competitive in Moldmaking

Continued training helps moldmakers make tooling decisions and properly use the latest cutting tool to efficiently machine high-quality molds.

Read More