Manufacturing Solutions: Wait ‘Til Next Year

As 2010 comes to a close, Americans are still struggling with a high unemployment rate, low consumer confidence, declining house prices and an uncomfortably high level of uncertainty about the future.

Share

Read Next

As 2010 comes to a close, Americans are still struggling with a high unemployment rate, low consumer confidence, declining house prices and an uncomfortably high level of uncertainty about the future. However to be fair, the manufacturing sector did improve when compared with last year, especially the plastics industry. Total output of plastics products expanded by 7 percent in 2010, and shipments of new plastics machinery jumped by 50 percent through the first three quarters. But we are still far below the output levels we enjoyed prior to the recession, and there is a definite feeling that market demand for molded products is far from hitting on all cylinders.

The next 12 months will certainly be a challenge, but if moldmakers and molders can hold on until this time next year, then the economic fundamentals and market prospects will improve substantially in 2012 and beyond. Total real GDP growth will be 3 percent in 2011, with slower gains at the beginning and then the expansion will accelerate during the second half. In 2012, real GDP growth will be closer to 5 percent.

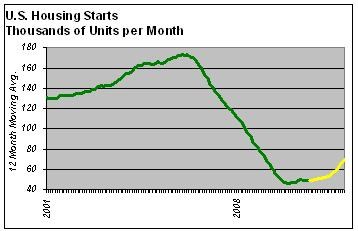

The good news is that we will not have to wait a whole year before we know if this forecast is accurate. The key to righting the U.S. economy is house prices and activity levels in residential construction and real estate. The failure of the housing market is what got us into this mess, and the correction will be the signal that the economy is back on track. Data on foreclosure sales, housing prices and construction activity are compiled and reported monthly, so if trends in these data start to rise then we should take heart.

For the first time in five years, the housing starts data will stop contracting and will contribute a modest amount to overall economic growth in 2010. This growth rate will accelerate in 2011, but the gains will be moderate by historical standards. Construction activity will not drive economic growth the way it did before the Great Recession, but it an uptrend in the construction and real estate markets will signal the return to a self-sustaining economic expansion.

The foreclosure sales data are particularly important in the coming months because foreclosures are weighing heavily on house prices. House prices are important to the overall economy for three reasons: (1) The wealth effect. About two-thirds of all Americans own their house, and for many of them, their house is their largest asset. When the value of houses declines consumers tend to spend less because they feel less wealthy; (2) When house prices are declining banks are less willing to lend money to small business owners who are offering their houses as collateral; and, (3) Many types of local governments are financed by property taxes, and when house prices decline, tax revenue is diminished. When combined, local governments are the country’s largest employer, and when tax revenues decline then teachers, police, road crews and public works employees lose their jobs. So, this economy does not work very well when house prices are declining, or even when there is uncertainty about whether they will fall.

The good news is that the foreclosure mess is gradually getting cleaned up, and after another year or so, house values will start to appreciate slowly in the vast majority of American markets. Until then, the manufacturing sector will continue to be a driver of economic growth in this country. As I have said before, our manufacturing sector will prove to be the primary hope for long-term salvation for the resumption of the American Dream. In the coming months, I will use this column to offer some new, and perhaps controversial, ideas and solutions for promoting and re-building our manufacturing dominance. I personally can’t wait ‘til next year … so I will start next month.

Related Content

ICYMI--MMT Chats: What's Happening to Our Industry? Time to Take a Stand for Plastics

MoldMaking Technology Editorial Director Christina Fuges chats with Bob Schiavone, Global Marketing Director for R&D/Leverage about his passion for manufacturing, marketing and the mission to change the perception of plastics. This episode is brought to you by ISCAR with New Ideas for Machining Intelligently.

Read More

MMT Chats: Impressions and Inspirations from AMBA Event that “Shifts the View”

MoldMaking Technology Editorial Director and Managing Editor share their takeaways from a recent American Mold Builders Association Conference focused on leadership and mentorship in the moldmaking community. This episode is brought to you by ISCAR with New Ideas for Machining Intelligently.

Read More

MMT Chats: Marketing’s Impact on Mold Manufacturing

Kelly Kasner, Director of Sales and Marketing for Michiana Global Mold (MGM) talks about the benefits her marketing and advertising, MGM’s China partnership and the next-generation skills gap. This episode is brought to you by ISCAR with New Ideas for Machining Intelligently.

Read More

MMT Chats: Simple Steps to Get Your Social Media Campaign Started

MoldMaking Technology Editorial Director Christina Fuges catches up with Gail Now’s Chief Curiosity Officer Gail Robertson. We talk about the importance of using the curiosity tool to tell your stories as part of a marketing strategy that includes social media. This episode is brought to you by ISCAR with New Ideas for Machining Intelligently.

Read MoreRead Next

How to Use Strategic Planning Tools, Data to Manage the Human Side of Business

Q&A with Marion Wells, MMT EAB member and founder of Human Asset Management.

Read More

How to Use Continuing Education to Remain Competitive in Moldmaking

Continued training helps moldmakers make tooling decisions and properly use the latest cutting tool to efficiently machine high-quality molds.

Read More

Are You a Moldmaker Considering 3D Printing? Consider the 3D Printing Workshop at NPE2024

Presentations will cover 3D printing for mold tooling, material innovation, product development, bridge production and full-scale, high-volume additive manufacturing.

Read More