Moldmaking Index Extends Movement in Narrow Growth Range

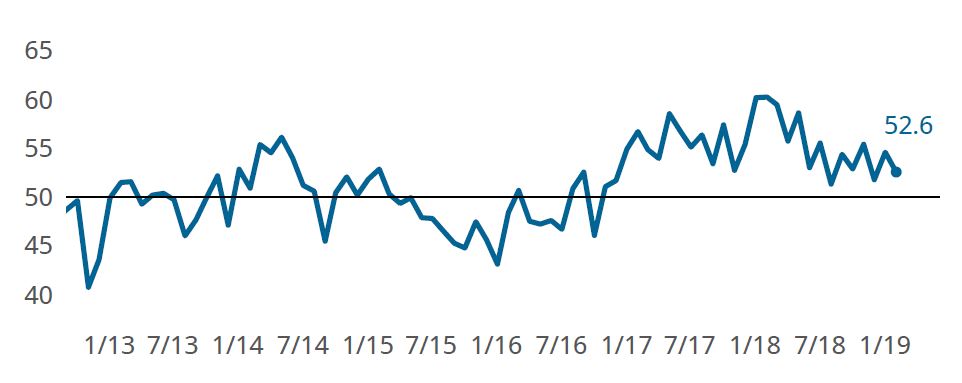

The Gardner Business Index (GBI): Moldmaking registered 52.6 in February, extending its narrow range of growth readings since September 2018, when it registered less than 200 basis points higher.

.jpg;width=70;height=70;mode=crop;format=webp)

Extended expansion in supplier deliveries, new orders, employment and production have kept the Moldmaking Index expanding since late 2016. The Index is currently experiencing its longest continuous expansion in recorded history.

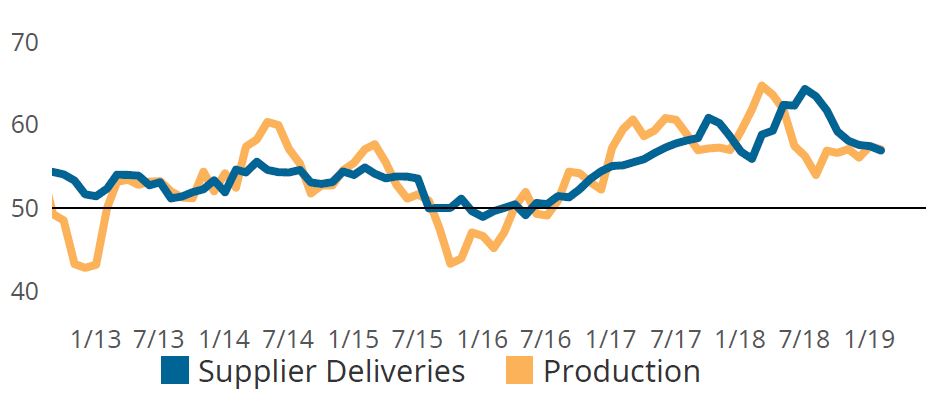

Supplier delivery and production readings since the start of the second half of 2018 suggest that the industry’s supply chain has adeptly rebalanced since experiencing a shock of new orders in early 2018, which caught suppliers with insufficient product volumes.

The Gardner Business Index (GBI): Moldmaking registered 52.6 in February, extending its narrow range of growth readings since September 2018, when it registered less than 200 basis points higher. Compared to the same month one year ago, the Index is down 13.7 percent; however, this comparison gauges the latest month’s data against the February 2018 record high reading of over 60.0. Gardner Intelligence’s review of the month’s underlying data reveals that supplier deliveries, production and backlog readings lifted the index — a calculated average of the components — higher. In contrast, new orders and backlogs pulled the Index lower. Only exports registered a contractionary reading during the month.

New orders and production both experienced slowing growth in February with the net resulting being an expansion in backlogs. Changes in the backlog reading are often attributed to the resulting ‘net’ movement in new orders and production. The slowing expansion in supplier deliveries beginning in the second-half of 2018 has resulted in supplier deliveries shadowing production readings in recent months. This suggests that the industry’s supply chain has adeptly rebalanced since experiencing a shock of new orders in early 2018, which caught suppliers with insufficient product volumes.

Related Content

-

Moldmaking Industry GBI Snuck Into Growth Territory in March

Growing for the first time since August 2022, the Gardner Business Index (GBI) Moldmaking ended March at 50.9, somewhat against the odds given the market developments that month.

-

Moldmaking Industry GBI Contracts for Four Months Straight

The GBI Moldmaking ended the month at 45.8, down one point from June, with components contracting or nearing contraction activity.

-

GBI: Moldmaking Undertakes Slightly Slowing Contraction

While most component activities remained unchanged in September, employment and supplier deliveries indicate a brief let-up from the contraction trend.