End Market Reports

Market Outlook: Motor Vehicles; Market Outlook: Aerospace Products and Parts

Market Outlook: Motor Vehicles

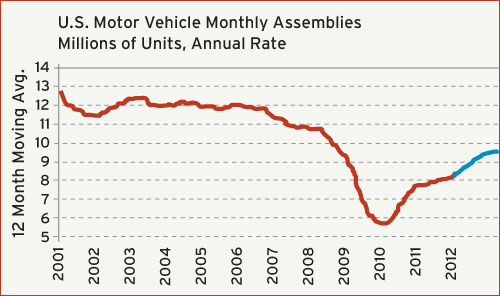

The total number of motor vehicles assembled in the U.S. registered a solid increase for the second consecutive year in 2011. After hitting a record-low level of only 5.7 million units in 2009, the number of assemblies in 2010 jumped 35% to 7.7 million units. In 2011, the number of assemblies escalated to 8.5 million units, which was a gain of 10%. Our forecast calls for another gain of 10% in 2012, and this would push the annual assemblies total to 9.5 million units.

Under normal circumstances, nobody would complain about a third straight year of double-digit growth, especially given the prevailing economic environment in the U.S. But as the accompanying chart illustrates, the U.S. motor vehicle industry is far from where it was prior to the last recession, and it will take several more years of growth in excess of 10% per annum to get us back to those levels. And as a wise man once said, “Who cares if the glass is half-full or half-empty … just fill it up.”

The average age of a car in America is 11 years. The value of the U.S. dollar is relatively low compared to the currencies of our major trading partners, and the price of gasoline is relatively high and rising. These are all strong reasons to expect solid growth in the global market demand for domestically-produced, fuel-efficient autos in the coming years. Unfortunately, the positive factors are mitigated by a high unemployment rate, slow income growth, low confidence, and increasing uncertainty amongst American consumers. So the activity levels for the U.S. auto industry will continue to rise at, at best, a moderate rate for the foreseeable future.

Market Outlook: Aerospace Products and Parts

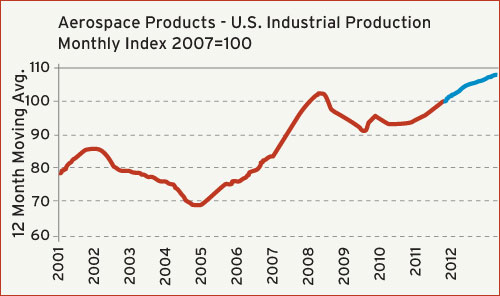

After a modest decline of just under 2% in 2010, total U.S. output of aerospace products escalated by a robust 8% in 2011. This industry is poised for another solid year of growth this year, and our current forecast calls for a gain of at least 6% in 2012. This sector did not suffer as badly as most others during the recession in ‘09, and the gains expected for this year will put total output above the pre-recession levels.

For the purposes of analysis, it is necessary to divide the aerospace industry into two categories: defense and non-defense. On the non-defense side, the expected increase in U.S. output is largely due to Boeing ramping up production of its new, fuel-efficient Dreamliner. The cost of jet fuel has jumped dramatically in recent years, and there is little reason to expect that this uptrend will not persist. And while there are a number of alternative fuels (electricity, propane, solar, etc.) under development that may ultimately prove viable for ground transportation, there are no new types of fuel in the pipeline for air transport. So planes must get more efficient. The good news for moldmakers is that more parts will be made from plastic and other composite materials in an effort to make planes lighter. The bad news is that this industry is so small that it is extremely difficult to enter the market if you are not already in it.

On the defense side, the fastest growing aerospace segment is un-manned aircraft (drones). These planes are cheaper to make, cheaper to operate, less dangerous to their pilots, and they are more effective at performing their tasks. The biggest knock against them is that they are maybe a little too effective, and their increased use also increases the risk of collateral damage. Nevertheless, military deployment of drones will continue to rise in the coming years. And sometime in the not-too-distant future, we can expect a sharp rise in civilian use of drones, particularly for law enforcement.

Related Content

Women Impacting Moldmaking

Honoring female makers, innovators and leaders who are influencing our industry's future.

Read More

Predictive Manufacturing Moves Mold Builder into Advanced Medical Component Manufacturing

From a hot rod hobby, medical molds and shop performance to technology extremes, key relationships and a growth strategy, it’s obvious details matter at Eden Tool.

Read More

The Role of Social Media in Manufacturing

Charles Daniels CFO of Wepco Plastics shares insights on the role of social media in manufacturing, how to improve the “business” side of a small mold shop and continually developing culture.

Read More

Transforming Moldmaking into Digital Industrial Manufacturing

Moldmaking and digitalization is at the core of this global industrial manufacturing company’s consolidation and diversification plan.

Read MoreRead Next

Reasons to Use Fiber Lasers for Mold Cleaning

Fiber lasers offer a simplicity, speed, control and portability, minimizing mold cleaning risks.

Read More

How to Use Strategic Planning Tools, Data to Manage the Human Side of Business

Q&A with Marion Wells, MMT EAB member and founder of Human Asset Management.

Read More

How to Use Continuing Education to Remain Competitive in Moldmaking

Continued training helps moldmakers make tooling decisions and properly use the latest cutting tool to efficiently machine high-quality molds.

Read More