End Market Reports: Automotive & Consumer Products

Automotive manufacturers may be hedging their output despite strong new order demand. Gardner Business Intelligence’s (GBI) review of consumer confidence, employment and credit markets all point to a strong 2017 for consumer spending.

.jpg;width=70;height=70;mode=crop;format=webp)

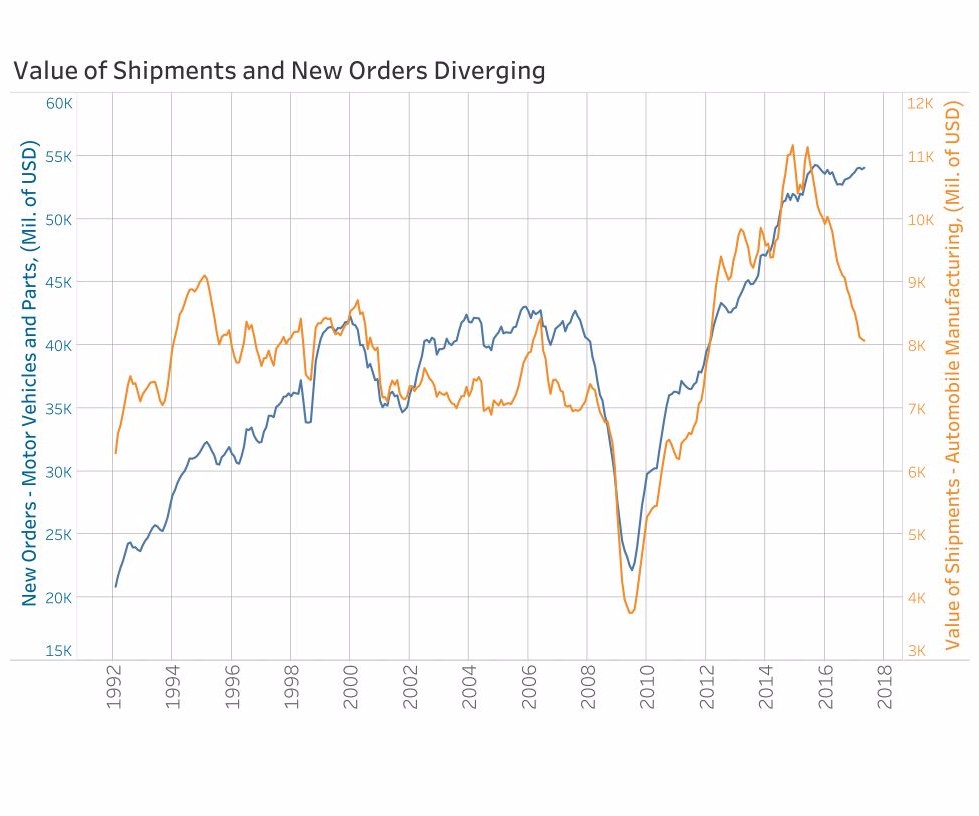

The value of shipments and new orders is diverging.

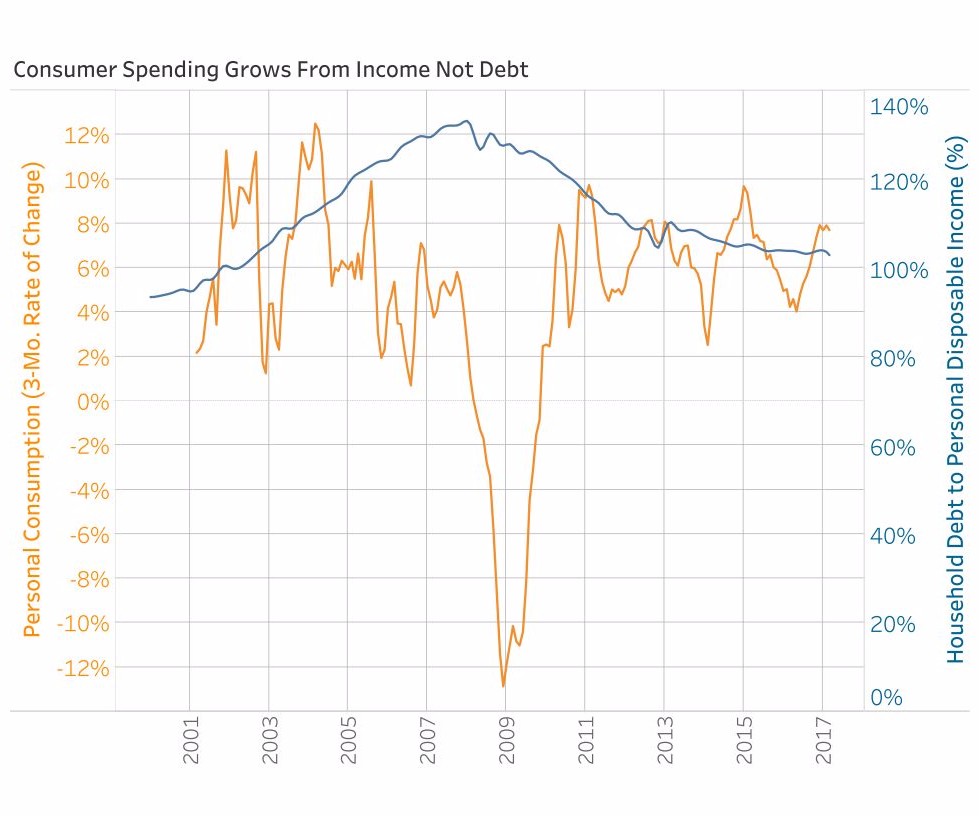

Consumer spending grows from income, not debt.

Automotive Shipment Values Falling Despite Strong New Orders

The annual rate of total vehicle sales nearly doubled between February 2009 and May 2015, increasing from 9.2 to 18.1 million units. This is an impressive feat for a pillar of the U.S. economy. The industry’s second notable feat was sustaining that hefty sales level for nearly two more years. Last year ended at an annualized production rate of 18.7 million units.

Automotive industry data shows a disconnect between the value of shipments, which has fallen sharply in the last year, and new orders. The 2017 average ratio of the value of new orders is 6.6x greater than shipments—one third higher than the average ratio since 1992 of 4.9x.

This means that the dollar value of new orders is more than six times greater than the value of concurrent shipments, the long-run ratio of which is 4.9. These results suggest that manufacturers may be hedging their output despite strong new order demand.

Among possible reasons for the pull back is the industry’s struggle to earn profits in the sedan and small car markets. According to J.D. Power, incentives in 2017 are expected to exceed $4,000, a near 15-percent increase over 2016 incentive levels. Automotive credit data shows several signs that give cause for concern as well. Because of the growing popularity and availability of 72- and 84-month duration automotive loans in recent years, more owners are finding themselves with negative equity in their vehicle, as the vehicle depreciates faster than their loan balance. The combination of low interest rates and lengthy loan durations make financing payments extremely affordable.

Consumer Metrics Point to a Strong Future

Gardner Business Intelligence’s (GBI) review of consumer confidence, employment and credit markets all point to a strong 2017 for consumer spending. Improved confidence in the economy has already yielded additional spending. Inflation-adjusted data for 2017 through April shows consumer spending on durable goods and total personal consumption increased by 4.9 percent and 7.2 percent, respectively. The increase in spending on durable goods is a result of growth in disposable personal income. The current ratio of household debt to personal disposable income at 103.2 percent is not significantly different than the 2015-2016 average of 104.1 percent.

Data from the Consumer Confidence Indexes measuring the present situation and future expectations both point to an economy of confident consumers. The index measuring the present situation, which increased sharply after the November presidential election, has continued to increase. For the first months of 2017, it averaged 137.9 as compared to 115.4 for the same period in 2016. Expectations data available through May 2017 indicate that consumer outlooks are significantly higher than for the same period in 2016. During the first five months of 2016, the index of Consumer Confidence Expectations averaged 81.4. By comparison, the index averaged 104.7 for the same period in 2017.

There is an opportunity for automotive original equipment manufacturers to continue producing at such elevated volumes. But, there are many financial factors that could constrict potential buyers from purchasing new vehicles in the future. It is for this reason that OEMs may be hedging their bets and holding back on shipment levels.

Related Content

Navigating Economic Resilience and Consumer Trends

Consumer behavior provides mold builders insight into the evolving market dynamics of goods and services that helps strategic planning.

Read More

Hammonton Mold, ADOP France Forge Strategic Partnership in Injection Blow Moldmaking

Hammonton Mold Inc., a leading full-service mold shop based in New Jersey specializing in injection blow molds (IBM), proudly announces its official partnership with ADOP France, a prominent IBM mold manufacturer based in Normandy, France.

Read More

MMT Chats: Applying Bench Lessons to the Business of Moldmaking

For this MMT Chat, my guest is Mark Gauvain, one of MMT’s newer Editorial Advisory Board members who has plenty to share as he recently made the move from working for some big manufacturers to working for himself as a consultant to moldmakers and molders on procurement and technology investment strategies.

Read More

How Hybrid Tooling Accelerates Product Development, Sustainability for PepsiCo

The consumer products giant used to wait weeks and spend thousands on each iteration of a prototype blow mold. Now, new blow molds are available in days and cost just a few hundred dollars.

Read MoreRead Next

End Market Reports: Computer and Medical

U.S. Computer Industry Emerging from Slump; Production of Medical Supplies and Equipment Is Accelerating

Read More

Are You a Moldmaker Considering 3D Printing? Consider the 3D Printing Workshop at NPE2024

Presentations will cover 3D printing for mold tooling, material innovation, product development, bridge production and full-scale, high-volume additive manufacturing.

Read More

How to Use Continuing Education to Remain Competitive in Moldmaking

Continued training helps moldmakers make tooling decisions and properly use the latest cutting tool to efficiently machine high-quality molds.

Read More