End Market Report: Automotive and Consumer, May 2013

Solid Year Expected for Automotive; Solid Year Expected for Automotive

Solid Year Expected for Automotive

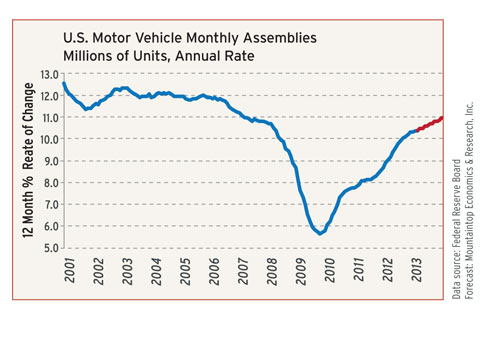

Our latest forecast calls for total motor vehicle assemblies in the US to reach 11.0 million units in 2013 which will represent a 7% annual. For the record, there were 10.3 million units assembled in 2012, and this was a jump of nearly 20% when compared with the total from 2011. As the chart below illustrates, 2013 is expected to be the fourth consecutive year in which this sector has experienced solid growth. And if our forecast for 2013 is correct, total assemblies in the US will still be one million units shy of their pre-recession level which consistently hit about 12 million units per year.

The average age of all of the motor vehicles in the US is still quite high by historical standards. So there is pent-up demand from consumers and small businesses who are awaiting better economic conditions. We expect the overall economy to grow by 2.5% this year and 3.5% next year. This trend of gradual improvement will be sufficient to foster steady growth in motor vehicle demand for the foreseeable future. The US market’s ever-rising awareness of the issues pertaining to energy independence and carbon emissions will continue to spur demand for lighter, more fuel-efficient vehicles and also vehicles that use non-traditional power sources such as natural gas, bio-diesel, and electricity.

There will be rising demand for small trucks and utility vehicles from contractors and other construction workers generated by the accelerating recovery in the residential construction sector. Until last year, the construction sector was a drag on overall economic activity. But this trend was clearly reversed in the second half of 2012, which means that a proper economic recovery can now finally start to unfold. Trends in the housing market are a primary factor in rising household wealth, and also in improving access to credit for most consumers and small businesses.

Output of Consumer Goods Still Underperforming

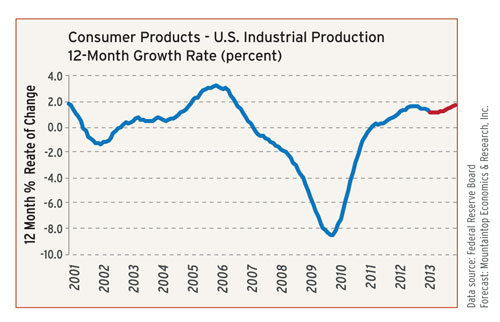

Total US industrial production of household consumer goods (excluding high-tech, autos, and energy) is forecast to expand 1.7% in 2013. This follows an increase of 1.4% in 2012. These rates are lower than the overall rate of growth in the US economy. Total GDP, after adjusting for inflation, grew by 2.2% in 2012, and we expect it to increase by 2.5% in 2013. Historical analysis indicates that growth in demand for consumer goods correlates closely with growth in the overall economy. The slower growth in US consumer goods production in recent years is due to the fact that many types of these goods are still being imported.

The problem with imports and our overall trade deficit in consumer products will take a long time to solve, but there are several near-term factors that will also affect US manufacturers this year. The most obvious are the persistent trends of agonizingly slow growth in both new job creation and personal incomes. The lackluster labor market has resulted in a decline in overall labor force. It will take at least another year or two before we get more robust improvement in the employment data. Until then, gains in consumer spending for all types of goods will be constrained.

Another short-term negative factor is the recent dip in consumer confidence that is due to the problems emanating from policymakers in Washington DC and the recent rise in payroll taxes. It will take a few months for most middle-class households to adjust to the fact that their paychecks are now a couple of hundred bucks lighter each pay period. Some of this direct hit to consumer pocketbooks might eventually be mitigated by lower energy prices or rising home values, but for at least the first half of this year it will curtail their spending on consumer goods.

Related Content

Women Impacting Moldmaking

Honoring female makers, innovators and leaders who are influencing our industry's future.

Read More

Transforming Moldmaking into Digital Industrial Manufacturing

Moldmaking and digitalization is at the core of this global industrial manufacturing company’s consolidation and diversification plan.

Read More

MMT Chats: Marketing’s Impact on Mold Manufacturing

Kelly Kasner, Director of Sales and Marketing for Michiana Global Mold (MGM) talks about the benefits her marketing and advertising, MGM’s China partnership and the next-generation skills gap. This episode is brought to you by ISCAR with New Ideas for Machining Intelligently.

Read More

Predictive Manufacturing Moves Mold Builder into Advanced Medical Component Manufacturing

From a hot rod hobby, medical molds and shop performance to technology extremes, key relationships and a growth strategy, it’s obvious details matter at Eden Tool.

Read MoreRead Next

Medical Equipment and Supplies; Consumer Goods End Market Report 2012

Medical Equipment and Supplies; Consumer Goods.

Read More

Are You a Moldmaker Considering 3D Printing? Consider the 3D Printing Workshop at NPE2024

Presentations will cover 3D printing for mold tooling, material innovation, product development, bridge production and full-scale, high-volume additive manufacturing.

Read More

How to Use Strategic Planning Tools, Data to Manage the Human Side of Business

Q&A with Marion Wells, MMT EAB member and founder of Human Asset Management.

Read More