Automotive & Consumer Products End Market Report 2012

Automotive & Consumer Products

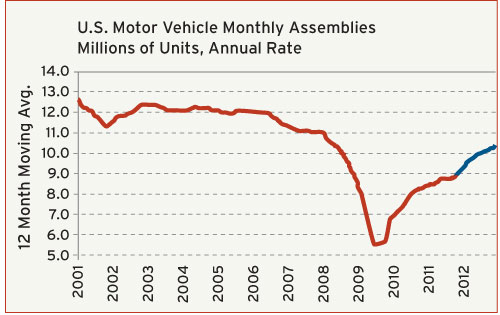

Automotive Sector Gaining Speed

Solid gains in the monthly data from the first quarter have caused us to raise our forecast for the number of motor vehicles that will be assembled in the U.S. for the year as a whole. The latest forecast calls for a total of a least 10 million assemblies in 2012. This is a robust gain of 15% from the total number of assemblies in 2011, but as the chart illustrates, it still leaves the industry about 2 million assemblies per year short of the annual figures prior to the recession.

The auto industry is currently benefiting from pent-up consumer demand, a market shift towards more efficient autos due to high gasoline prices, and a gradually improving economy. We expect these conditions to persist for the remainder of this year and through 2013. However, there are downside risks to this forecast. The unemployment rate is still too high, and the current rate of economic growth is not yet sufficient to generate more rapid improvement in the jobless numbers. And if it continues unabated, the rising cost of gasoline may dampen sentiment and put a more severe pinch on consumer spending behavior. The payroll tax cut is scheduled to expire at the end of 2012, and this too could put a drag on the market for new cars in 2013 if conditions fail to meet expectations by this year’s end.

As of right now, the most likely outcome is that the markets and policymakers will find a favorable resolution to all of these issues and the recovery will remain intact. But we invite all moldmakers to monitor the trends in these data just to make sure that there are no significant changes to this outlook.

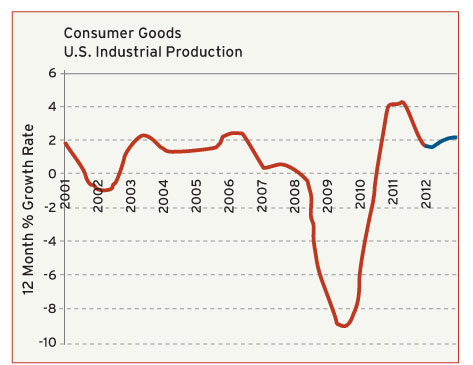

Output of Consumer Products Still Rising, but Growth Rate Decelerates

The total U.S. production of consumer products remains in an uptrend, but the rate of growth has decelerated in recent months. Total output expanded by 1% in the first quarter of this year when compared to the same quarter a year earlier. This is slower than the 2% rate of growth this sector registered for the entire year of 2011. Our forecast calls for the growth rate to nudge back up to the 2% level by this year’s end. For historical context, a gain of 2% this year would still leave total output of consumer goods about 5% below the pre-recession peak it hit in 2007.

Demand for many of the products in this category follows the trends in residential construction and real estate, and these sectors are just barely into their early recovery phase. We expect the total number of housing starts to increase by 15% in 2012, but this gain follows three years of virtually no advance from historically depressed levels. It will take at least another two years for construction and real estate activity to return to “normal” levels, and this will restrict demand for some consumer products.

For those products that are not tied to construction, the next 12 months should be good, but not great. Unemployment levels will remain high, and this will result in stagnant income growth for most middle-class households. Household formations and the overall population will gradually increase, and this will put a floor under the demand for consumer products. There will also be a gradual increase in the number of these products that are “reshored” from the so-called low-cost manufacturers overseas. Unfortunately, these gains will be more than offset by the rapid rise in materials costs for manufacturers of these products. Overall, the net outcome will be a rather pedestrian rate of expansion in these markets.

Related Content

OEE Monitoring System Addresses Root Cause of Machine Downtime

Unique sensor and patent-pending algorithm of the Amper machine analytics system measures current draw to quickly and inexpensively inform manufacturers which machines are down and why.

Read More

Making Quick and Easy Kaizen Work for Your Shop

Within each person is unlimited creative potential to improve shop operations.

Read More

Mold Design Review: The Complete Checklist

Gerardo (Jerry) Miranda III, former global tooling manager for Oakley sunglasses, reshares his complete mold design checklist, an essential part of the product time and cost-to-market process.

Read More

Tackling a Mold Designer Shortage

Survey findings reveal a shortage of skilled mold designers and engineers in the moldmaking community, calling for intervention through educational programs and exploration of training alternatives while seeking input from those who have addressed the issue successfully.

Read MoreRead Next

End Market Report: Aerospace/Defense & Packaging

Plastics Packaging Outlook: Moderate Growth in 2012, and Aerospace/Defense Spending Outlook.

Read More

How to Use Strategic Planning Tools, Data to Manage the Human Side of Business

Q&A with Marion Wells, MMT EAB member and founder of Human Asset Management.

Read More

Reasons to Use Fiber Lasers for Mold Cleaning

Fiber lasers offer a simplicity, speed, control and portability, minimizing mold cleaning risks.

Read More